Electronic components distributor Avnet (NASDAQGS:AVT) met Wall Street’s revenue expectations in Q1 CY2025, but sales fell by 6% year on year to $5.32 billion. On the other hand, next quarter’s revenue guidance of $5.3 billion was less impressive, coming in 3.3% below analysts’ estimates. Its non-GAAP profit of $0.84 per share was 17.6% above analysts’ consensus estimates.

Is now the time to buy Avnet? Find out by accessing our full research report, it’s free.

Avnet (AVT) Q1 CY2025 Highlights:

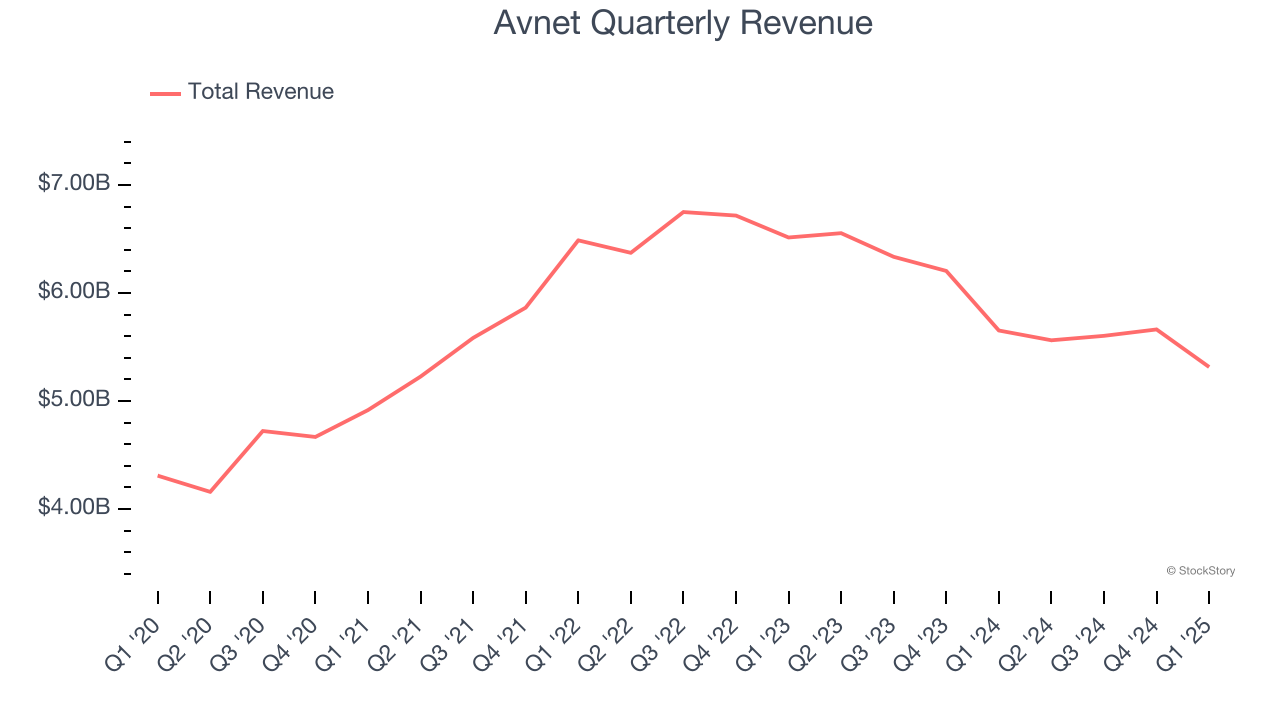

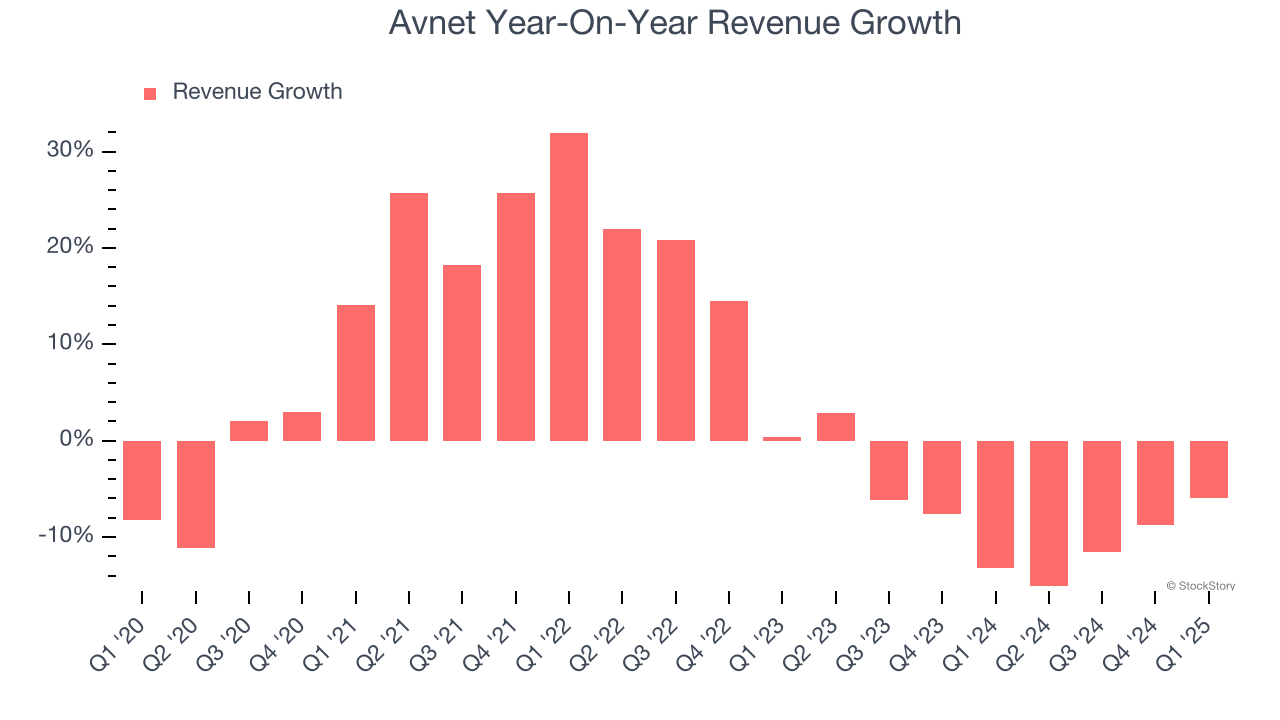

- Revenue: $5.32 billion vs analyst estimates of $5.29 billion (6% year-on-year decline, in line)

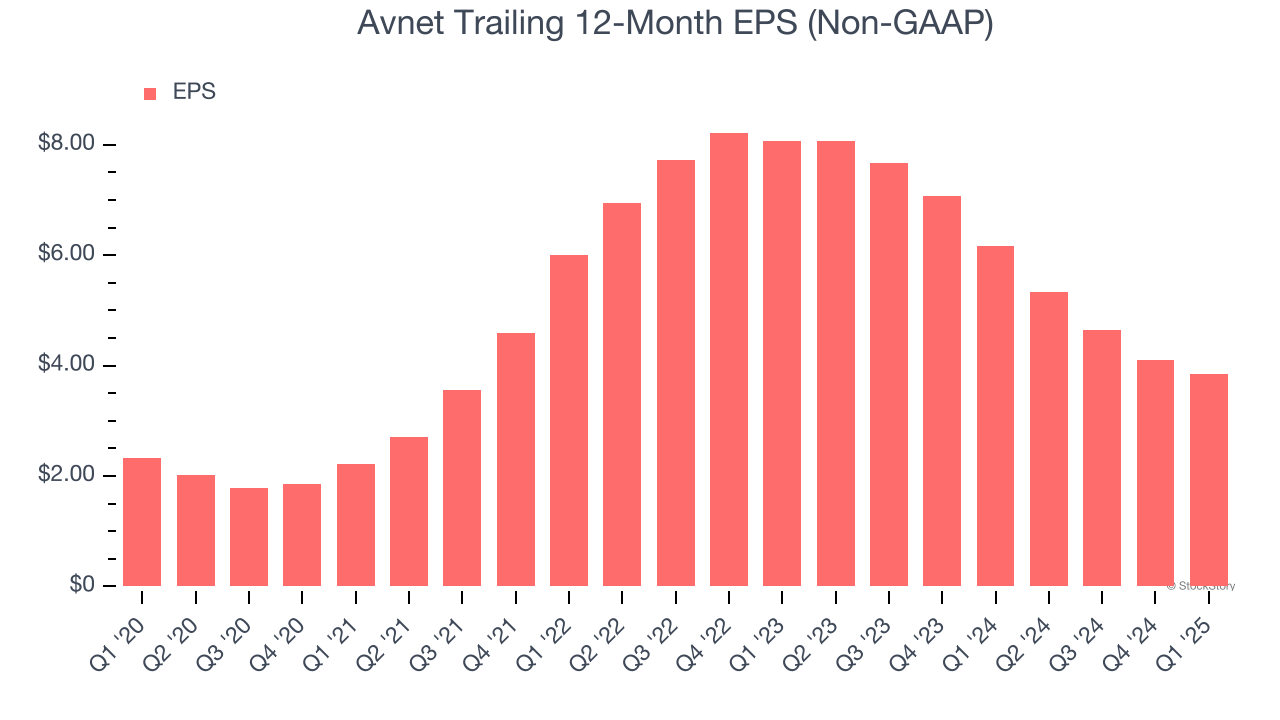

- Adjusted EPS: $0.84 vs analyst estimates of $0.71 (17.6% beat)

- Adjusted EBITDA: $169.1 million vs analyst estimates of $161.6 million (3.2% margin, 4.7% beat)

- Revenue Guidance for Q2 CY2025 is $5.3 billion at the midpoint, below analyst estimates of $5.48 billion

- Adjusted EPS guidance for Q2 CY2025 is $0.70 at the midpoint, below analyst estimates of $0.90

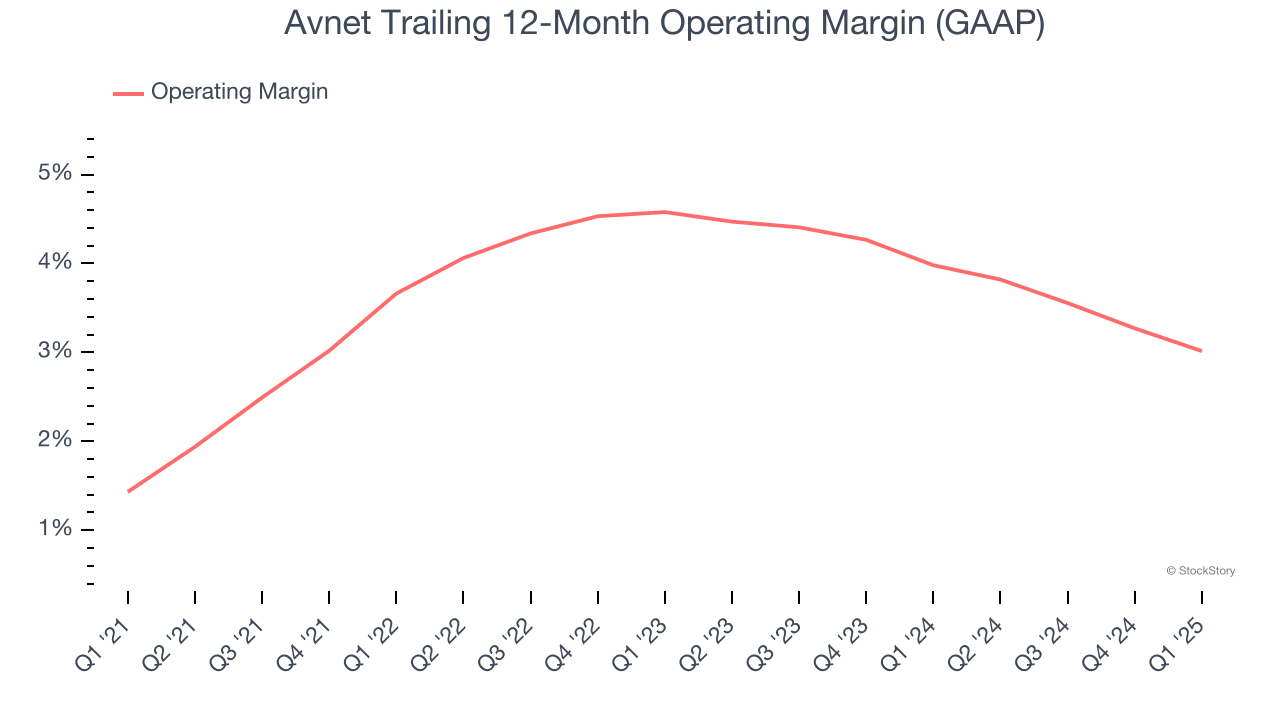

- Operating Margin: 2.7%, down from 3.7% in the same quarter last year

- Free Cash Flow Margin: 2.1%, down from 8.1% in the same quarter last year

- Market Capitalization: $4.43 billion

“We are pleased with our third quarter results, with revenue and earnings exceeding our expectations,” said Avnet Chief Executive Officer Phil Gallagher.

Company Overview

With a century-long history of adapting to technological evolution, Avnet (NASDAQ:AVT) is a global electronic components distributor that connects manufacturers of semiconductors and other electronic parts with businesses that need these components.

Sales Growth

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years.

With $22.15 billion in revenue over the past 12 months, Avnet is a behemoth in the business services sector and benefits from economies of scale, giving it an edge in distribution. This also enables it to gain more leverage on its fixed costs than smaller competitors and the flexibility to offer lower prices. However, its scale is a double-edged sword because it’s harder to find incremental growth when you’ve penetrated most of the market. To accelerate sales, Avnet likely needs to optimize its pricing or lean into new offerings and international expansion.

As you can see below, Avnet’s sales grew at a mediocre 4.1% compounded annual growth rate over the last five years. This shows it couldn’t generate demand in any major way and is a tough starting point for our analysis.

Long-term growth is the most important, but within business services, a half-decade historical view may miss new innovations or demand cycles. Avnet’s performance shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 8.3% annually.

This quarter, Avnet reported a rather uninspiring 6% year-on-year revenue decline to $5.32 billion of revenue, in line with Wall Street’s estimates. Company management is currently guiding for a 4.7% year-on-year decline in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 3% over the next 12 months. Although this projection implies its newer products and services will catalyze better top-line performance, it is still below the sector average.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. Click here to access our free report one of our favorites growth stories.

Operating Margin

Avnet was profitable over the last five years but held back by its large cost base. Its average operating margin of 3.5% was weak for a business services business.

On the plus side, Avnet’s operating margin rose by 1.6 percentage points over the last five years, as its sales growth gave it operating leverage.

In Q1, Avnet generated an operating profit margin of 2.7%, down 1 percentage points year on year. This reduction is quite minuscule and indicates the company’s overall cost structure has been relatively stable.

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Avnet’s EPS grew at a remarkable 10.5% compounded annual growth rate over the last five years, higher than its 4.1% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

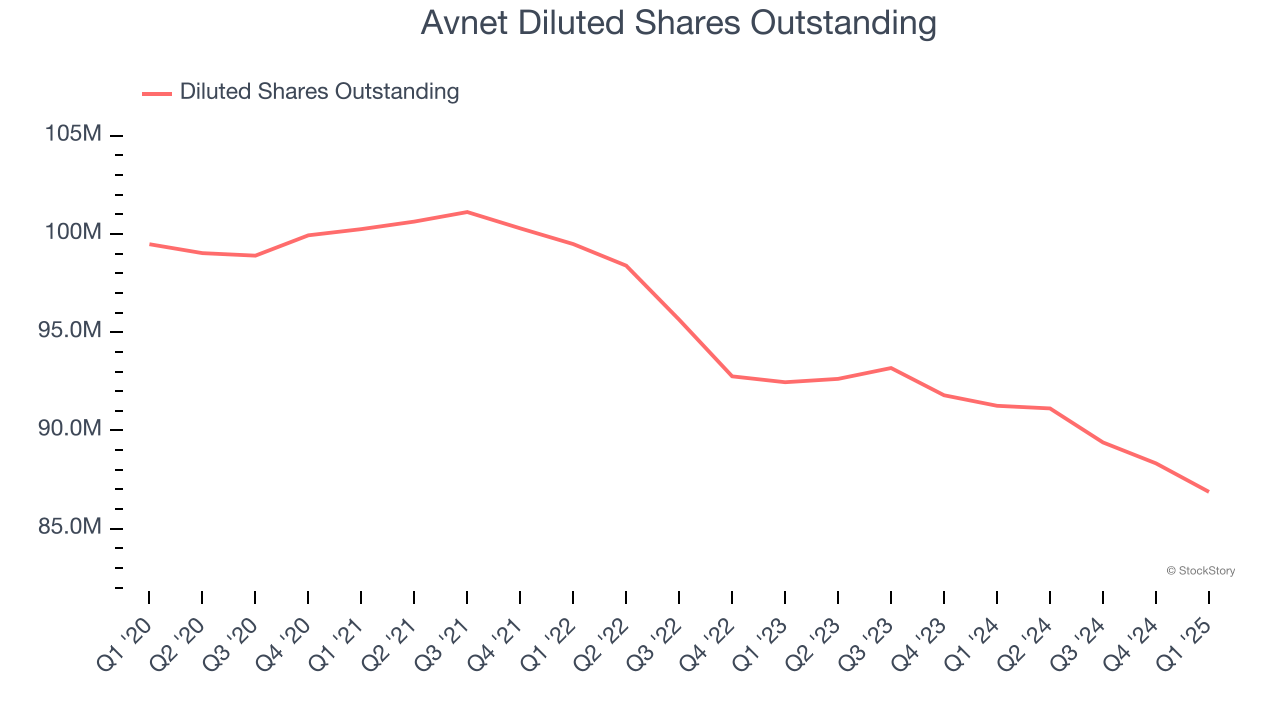

Diving into the nuances of Avnet’s earnings can give us a better understanding of its performance. As we mentioned earlier, Avnet’s operating margin declined this quarter but expanded by 1.6 percentage points over the last five years. Its share count also shrank by 12.7%, and these factors together are positive signs for shareholders because improving profitability and share buybacks turbocharge EPS growth relative to revenue growth.

In Q1, Avnet reported EPS at $0.84, down from $1.10 in the same quarter last year. Despite falling year on year, this print easily cleared analysts’ estimates. Over the next 12 months, Wall Street expects Avnet’s full-year EPS of $3.85 to grow 32.5%.

Key Takeaways from Avnet’s Q1 Results

We were impressed by how significantly Avnet blew past analysts’ EPS and EBITDA expectations this quarter. On the other hand, its revenue and EPS guidance for next quarter fell short of Wall Street’s estimates. Overall, this quarter could have been better. The stock traded down 7.3% to $47.50 immediately after reporting.

Avnet’s latest earnings report disappointed. One quarter doesn’t define a company’s quality, so let’s explore whether the stock is a buy at the current price. When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.