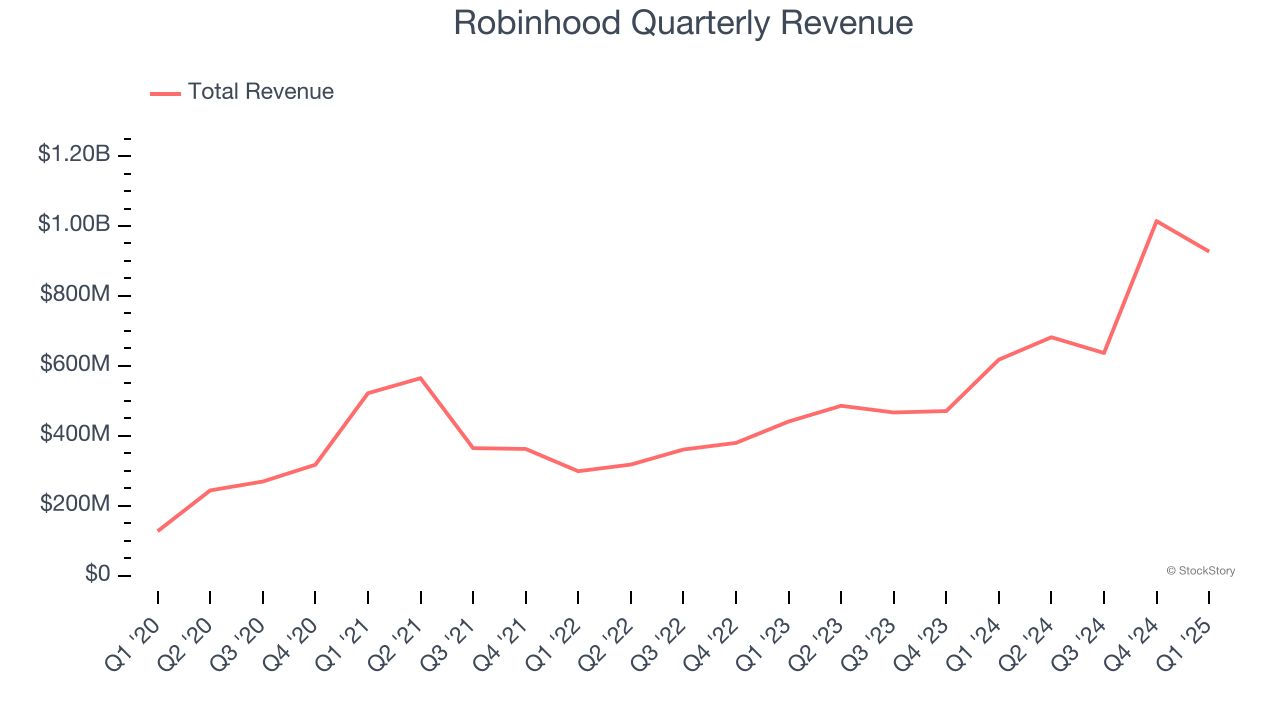

Financial services company Robinhood (NASDAQ:HOOD) announced better-than-expected revenue in Q1 CY2025, with sales up 50% year on year to $927 million. Its GAAP profit of $0.37 per share was 13.5% above analysts’ consensus estimates.

Is now the time to buy Robinhood? Find out by accessing our full research report, it’s free.

Robinhood (HOOD) Q1 CY2025 Highlights:

- Revenue: $927 million vs analyst estimates of $915.7 million (50% year-on-year growth, 1.2% beat)

- EPS (GAAP): $0.37 vs analyst estimates of $0.33 (13.5% beat)

- Adjusted EBITDA: $470 million vs analyst estimates of $490.5 million (50.7% margin, 4.2% miss)

- Operating Margin: 40%, up from 25.6% in the same quarter last year

- Free Cash Flow was $631 million, up from -$1.41 billion in the previous quarter

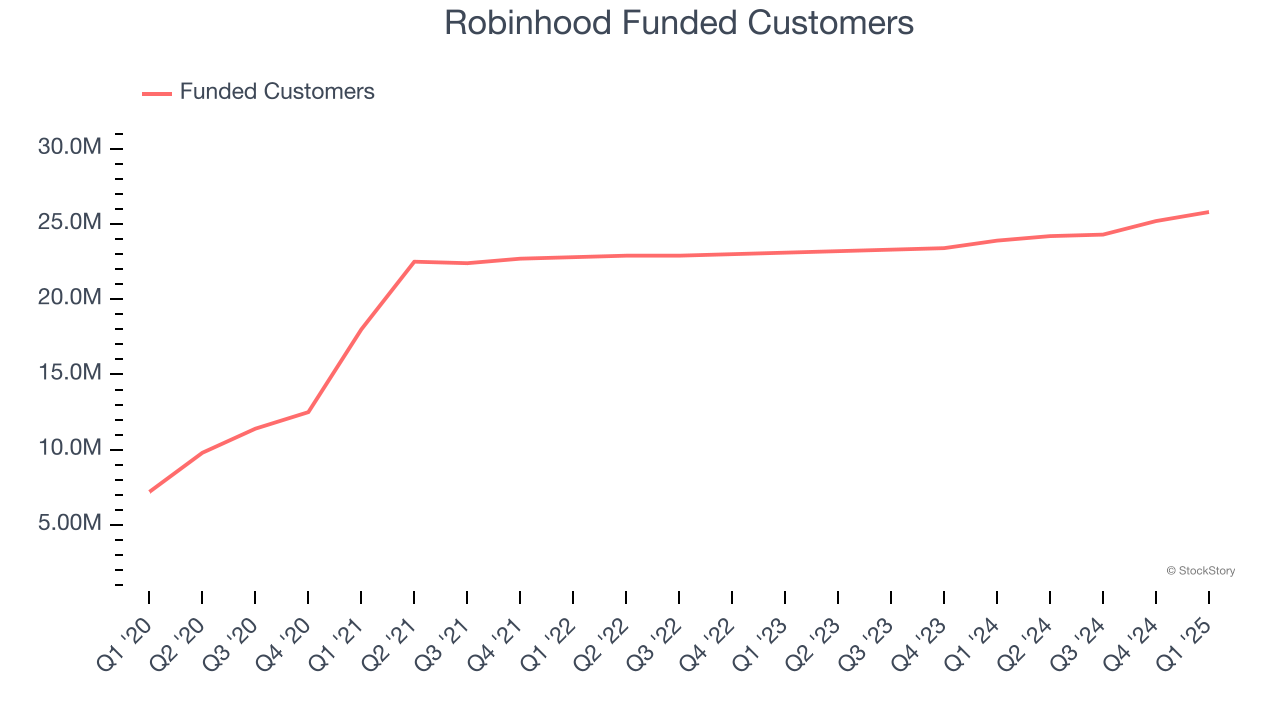

- Funded Customers: 25.8 million, up 1.9 million year on year

- Market Capitalization: $43.72 billion

“This quarter, we significantly accelerated product innovation across our key initiatives, highlighted by the announcement of Robinhood Strategies, Banking, and Cortex,” said Vlad Tenev, Chair and CEO of Robinhood.

Company Overview

With a mission to democratize finance, Robinhood (NASDAQ:HOOD) is an online consumer finance platform known for its commission-free stock and crypto trading.

Financial Technology

Financial technology companies benefit from the increasing consumer demand for digital payments, banking, and finance. Tailwinds fueling this trend include e-commerce along with improvements in blockchain infrastructure and AI-driven credit underwriting, which make access to money faster and cheaper. Despite regulatory scrutiny and resistance from traditional financial institutions, fintechs are poised for long-term growth as they disrupt legacy systems by expanding financial services to underserved population segments.

Sales Growth

A company’s long-term sales performance can indicate its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Over the last three years, Robinhood grew its sales at an exceptional 27% compounded annual growth rate. Its growth surpassed the average consumer internet company and shows its offerings resonate with customers, a great starting point for our analysis.

This quarter, Robinhood reported magnificent year-on-year revenue growth of 50%, and its $927 million of revenue beat Wall Street’s estimates by 1.2%.

Looking ahead, sell-side analysts expect revenue to grow 13.1% over the next 12 months, a deceleration versus the last three years. Still, this projection is commendable and implies the market is forecasting success for its products and services.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Funded Customers

User Growth

As a fintech company, Robinhood generates revenue growth by increasing both the number of users on its platform and the number of transactions they execute.

Over the last two years, Robinhood’s funded customers, a key performance metric for the company, increased by 4.1% annually to 25.8 million in the latest quarter. This growth rate lags behind the hottest consumer internet applications. If Robinhood wants to accelerate growth, it likely needs to engage users more effectively with its existing offerings or innovate with new products.

In Q1, Robinhood added 1.9 million funded customers, leading to 7.9% year-on-year growth. The quarterly print was higher than its two-year result, suggesting its new initiatives are accelerating user growth.

Revenue Per User

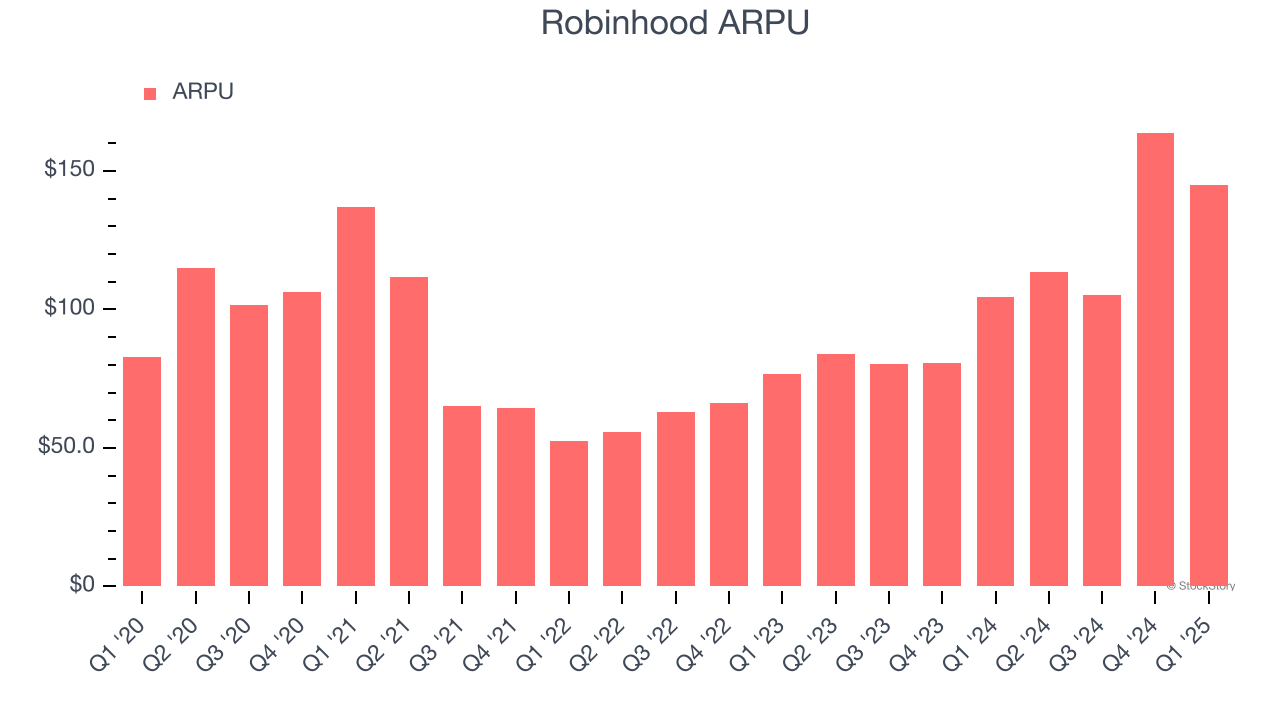

Average revenue per user (ARPU) is a critical metric to track because it measures how much the company earns in fees from each user. ARPU also gives us unique insights into the average transaction size on Robinhood’s platform and the company’s take rate, or "cut", on each transaction.

Robinhood’s ARPU growth has been exceptional over the last two years, averaging 43%. Its ability to increase monetization while growing its funded customers demonstrates its platform’s value, as its users are spending significantly more than last year.

This quarter, Robinhood’s ARPU clocked in at $145. It grew by 38.7% year on year, faster than its funded customers.

Key Takeaways from Robinhood’s Q1 Results

It was good to see Robinhood top analysts’ revenue and EPS expectations this quarter. On the other hand, its EBITDA missed. Overall, this quarter was mixed. The stock remained flat at $48.89 immediately following the results.

Robinhood underperformed this quarter, but does that create an opportunity to invest right now? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.