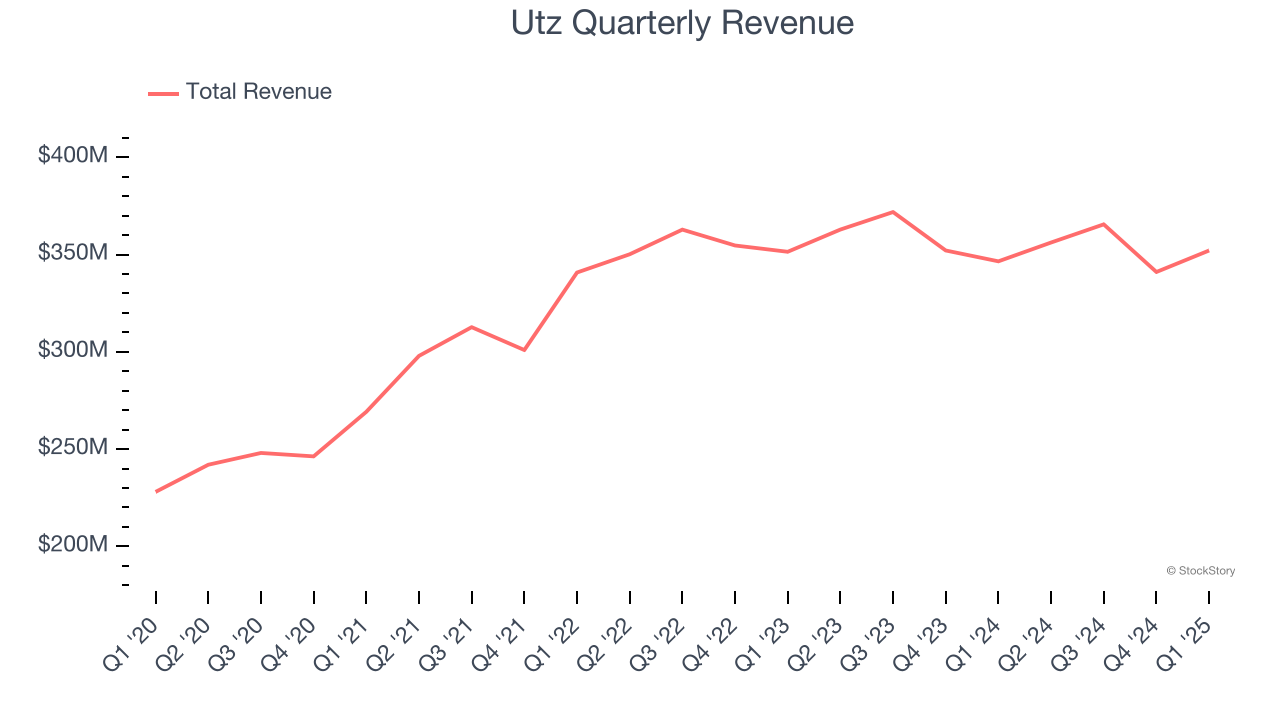

Snack food company Utz Brands (NYSE:UTZ) beat Wall Street’s revenue expectations in Q1 CY2025, with sales up 1.6% year on year to $352.1 million. Its non-GAAP profit of $0.16 per share was in line with analysts’ consensus estimates.

Is now the time to buy Utz? Find out by accessing our full research report, it’s free.

Utz (UTZ) Q1 CY2025 Highlights:

- Revenue: $352.1 million vs analyst estimates of $350.2 million (1.6% year-on-year growth, 0.6% beat)

- Adjusted EPS: $0.16 vs analyst estimates of $0.15 (in line)

- Adjusted EBITDA: $45.1 million vs analyst estimates of $44.79 million (12.8% margin, 0.7% beat)

- Operating Margin: 1.6%, down from 2.8% in the same quarter last year

- Free Cash Flow was -$59.01 million compared to -$22.7 million in the same quarter last year

- Organic Revenue rose 2.9% year on year (1.5% in the same quarter last year)

- Market Capitalization: $1.14 billion

“I’m pleased with our strong start to the year, as we delivered nearly 3% Organic Net Sales growth(1), and gained dollar and pound share of the Salty Snacks category in the first quarter(2). Our use of bonus packs and focused trade promotions have been effective in addressing consumer value needs. We’ve now shown our ability to grow despite category softness, due to our unique geographic expansion opportunity. In addition, we delivered our ninth consecutive quarter of year-over-year Adjusted EBITDA Margin expansion, and we drove Adjusted Earnings Per Share growth of over 14%,” said Howard Friedman, Chief Executive Officer of Utz.

Company Overview

Tracing its roots back to 1921 when Bill and Salie Utz began making potato chips in their kitchen, Utz Brands (NYSE:UTZ) offers salty snacks such as potato chips, tortilla chips, pretzels, cheese snacks, and ready-to-eat popcorn, among others.

Sales Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but many enduring ones grow for years.

With $1.41 billion in revenue over the past 12 months, Utz is a small consumer staples company, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with retailers.

As you can see below, Utz’s 4.2% annualized revenue growth over the last three years was sluggish, but to its credit, consumers bought more of its products.

This quarter, Utz reported modest year-on-year revenue growth of 1.6% but beat Wall Street’s estimates by 0.6%.

Looking ahead, sell-side analysts expect revenue to grow 1.8% over the next 12 months, a slight deceleration versus the last three years. This projection doesn't excite us and indicates its products will see some demand headwinds.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link.

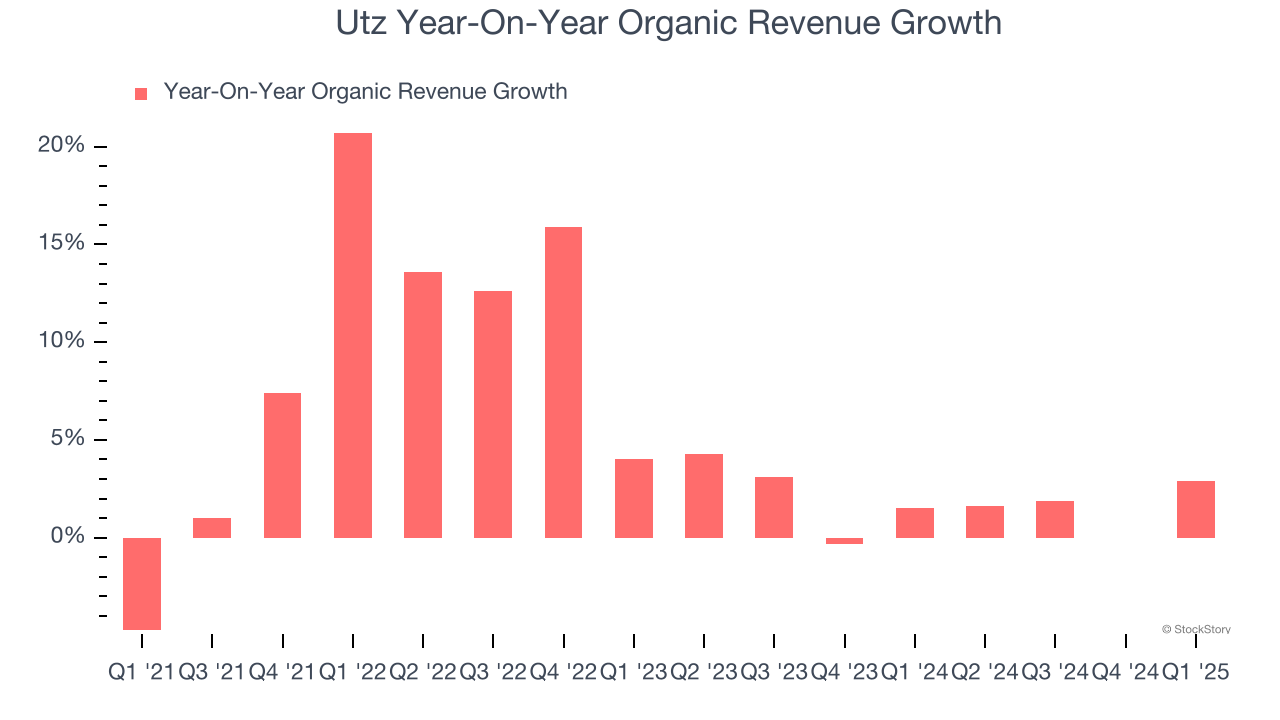

Organic Revenue Growth

When analyzing revenue growth, we care most about organic revenue growth. This metric captures a business’s performance excluding one-time events such as mergers, acquisitions, and divestitures as well as foreign currency fluctuations.

The demand for Utz’s products has been stable over the last eight quarters but fell behind the broader sector. On average, the company has posted feeble year-on-year organic revenue growth of 1.9%.

In the latest quarter, Utz’s organic sales rose by 2.9% year on year. This growth was an acceleration from its historical levels, which is always an encouraging sign.

Key Takeaways from Utz’s Q1 Results

This was a relatively in-line quarter, with key metrics such as revenue and EPS roughly meeting expectations. The stock remained flat at $13.20 immediately after reporting.

So do we think Utz is an attractive buy at the current price? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free.